To build vibe-coded insurance products that meet regulatory requirements in 2026, recognize that insurance is regulated state-by-state in the US (50 different regulators with overlapping but distinct rules), focus your initial compliance work on four areas (licensing, rate filing, consumer disclosure, data security), partner with a Managing General Agent or licensed carrier rather than seeking your own license, and accept that insurance compliance is fundamentally slower than other tech sectors. Most vibe-coded insurance products work via partnerships, not via direct licensing.

This piece walks through the four compliance areas, the partnership patterns that bypass direct licensing, the timeline expectations, and the four mistakes that get insurance startups shut down by regulators.

Why Insurance Is Different From Other Regulated Industries

Insurance regulation is uniquely complex among regulated industries. Each US state has its own insurance department with authority to regulate insurance products sold to its residents. A nationwide insurance product needs to navigate 50 distinct regulatory regimes, each with its own filing requirements, rate review processes, and disclosure rules.

This matters for vibe-coded insurance products because the regulatory complexity does not scale down for small builders. A startup selling insurance in 5 states still needs to comply with all 5 sets of rules. The compliance overhead is fixed; only revenue scales.

A 2025 Insurance Innovation Report tracked 200 insurance tech startups and found that those operating via Managing General Agent (MGA) partnerships reached market 14 months faster on average than startups pursuing their own carrier licenses. The MGA route adds revenue share costs but eliminates 12 to 18 months of regulatory navigation. For vibe-coded insurance products, the MGA partnership is almost always the right starting structure.

The pattern to copy is the way modern fintech startups partner with chartered banks rather than seeking their own bank charters. The bank charter is the highest-friction regulatory barrier; partnering with an existing chartered bank lets the fintech focus on product. Insurance follows the same pattern: the carrier license is the highest-friction barrier; partnering with an MGA or carrier eliminates it.

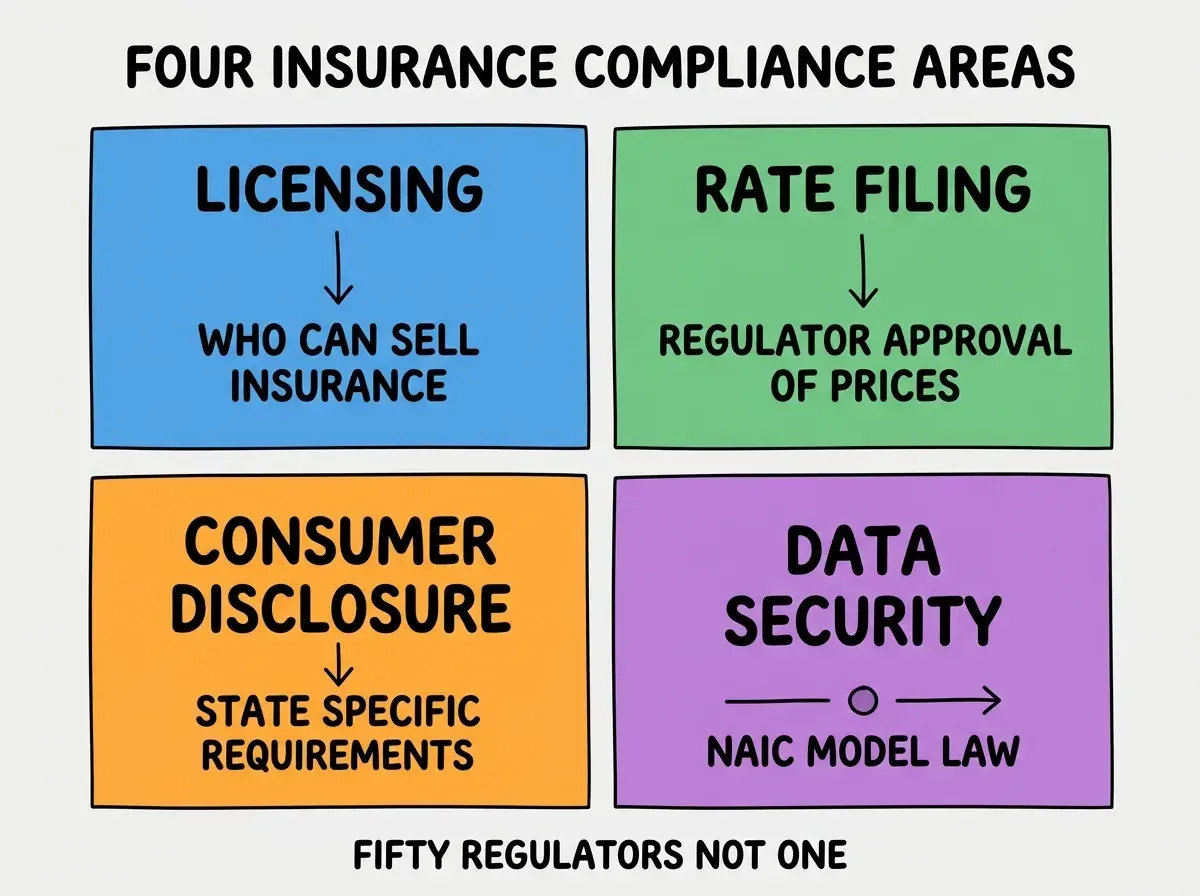

The Four Compliance Areas That Matter Most

Insurance compliance covers many areas. Four areas matter most for vibe-coded insurance products in their first year.

Area 1, licensing. Who is allowed to sell insurance? Almost certainly not your startup directly. Licensing is the threshold question that determines your business structure.

Area 2, rate filing. Insurance prices must be approved by state regulators in many product categories. Rate changes require new filings. The pricing process is dramatically slower than other industries.

Area 3, consumer disclosure. What information must be presented to consumers, how, when. Each state has specific requirements; some require physical mail, others allow digital, some require both.

Area 4, data security. The NAIC Insurance Data Security Model Law applies in most states. Specific requirements for data protection, breach notification, third-party vendor management.

The Partnership Patterns That Bypass Direct Licensing

Three partnership patterns let vibe-coded insurance products operate without direct carrier licensing.

Pattern 1, Managing General Agent (MGA). Partner with an MGA who has carrier relationships. You handle the technology and customer experience; the MGA handles the regulatory paperwork. Most common for insurance startups.

Browse more regulated industry guides

Read more pulse articlesPattern 2, white-label with licensed carrier. Carrier issues the policies under their license; your product is the customer-facing brand and technology. Higher complexity but more brand control.

Pattern 3, technology-only model. You sell software to licensed carriers and brokers; they handle insurance regulation directly. Lowest regulatory burden; lower margin per transaction.

The right pattern depends on your business model. Direct-to-consumer insurance startups usually need MGA partnerships; B2B insurance technology can stay in pattern 3.

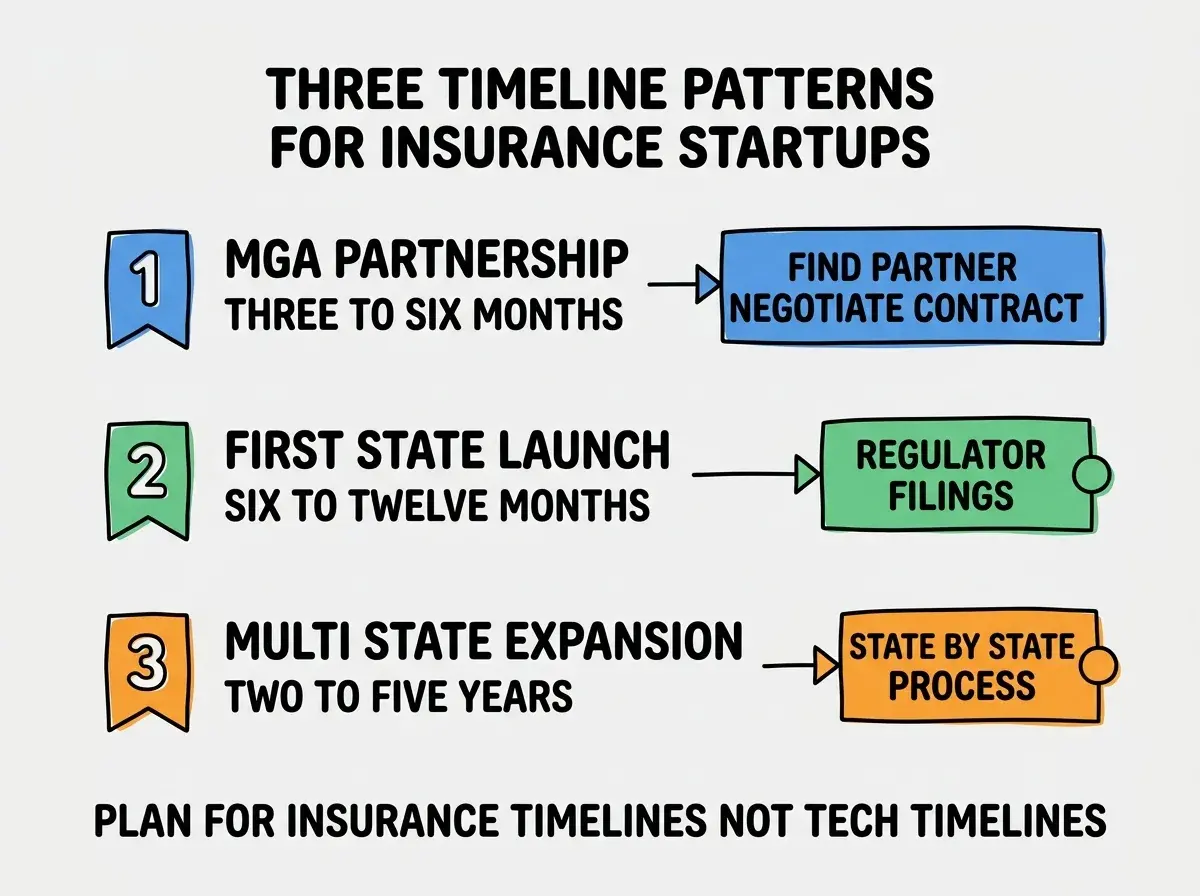

The Timeline Expectations

Insurance development timelines are dramatically longer than other tech sectors. Three timeline patterns hold across most insurance startups.

Timeline 1, MGA partnership. 3 to 6 months to find the right partner, negotiate terms, integrate technically. Faster than direct licensing but still slow.

Timeline 2, first state launch. 6 to 12 months from MGA contract to selling in your first state. Regulator filings, rate approvals, consumer disclosure documentation.

Timeline 3, multi-state expansion. 2 to 5 years to be live in 20+ states. Each state is its own regulatory process. National scale takes time.

These timelines surprise founders coming from other tech sectors. Plan accordingly; insurance is a marathon, not a sprint.

What Insurance Tech Can Do Quickly

Despite the long compliance timelines, three insurance tech opportunities have shorter paths to market.

Opportunity 1, broker tools. Software that helps existing licensed brokers be more efficient. Sells B2B to brokers; broker handles regulatory exposure. Can ship in months.

Opportunity 2, claims processing for carriers. Software that helps licensed carriers process claims faster or more accurately. B2B sales to carriers. Can ship in months.

Opportunity 3, embedded insurance via partnership. Adding insurance to non-insurance products (travel insurance on flight booking, gadget insurance on electronics) via carrier partnerships. Faster than direct insurance products.

The combination of these opportunities means there are insurance-adjacent paths that do not require multi-year compliance journeys. Pick the path based on your skills and goals.

The most damaging insurance startup mistake is launching a consumer insurance product without proper regulatory structure, hoping to "fix it later." State insurance regulators move fast on this kind of violation. Cease-and-desist letters arrive within weeks; fines and reputational damage can kill the startup before it has a chance to fix the structure. The fix is to engage insurance regulatory counsel before launching any insurance product. The legal fees are real but small compared to the cost of getting shut down. Insurance is one of the few areas where "ask forgiveness not permission" actively destroys businesses.

The other mistake is underestimating the customer service requirements of insurance products. Consumers expect human support for insurance questions in ways they do not for other digital products. Plan for human support staff from launch; pure-self-service insurance products consistently underperform on customer satisfaction and regulatory complaint rates.

Working With Insurance Regulatory Counsel

Insurance regulatory counsel is essential and surprisingly accessible. Three patterns make the relationship productive.

Pattern 1, retain counsel before launching. Find an insurance regulatory attorney before your first state filing. The upfront investment ($5K-15K) prevents far larger compliance costs.

Pattern 2, use specialized firms. Insurance regulatory law is specialized. Generalist business attorneys often miss the nuances. Look for firms with explicit insurance regulatory practice.

Pattern 3, build a multi-state strategy with counsel. Counsel can help prioritize which states to enter first based on regulatory complexity, market size, and your business model. The strategic input is as valuable as the legal work.

The cost of good regulatory counsel is real but small compared to the cost of compliance violations. Plan for it as a foundational expense rather than an optional add-on.

State-By-State Expansion Strategy

Multi-state expansion is the long-term challenge for insurance startups. Three patterns help structure the expansion.

Pattern A, start with friendly states. Some states (Texas, Florida, Arizona) have faster filing processes than others (California, New York). Launching in friendly states first builds momentum.

Pattern B, batch by region. Group neighboring states (Northeast, Southwest) for parallel filing efforts. Some efficiencies in marketing and operations come from regional clusters.

Pattern C, prioritize by market size. California and Texas alone are 20+ percent of the US insurance market. Hitting these states early is more impactful than expanding into smaller states.

The right expansion strategy depends on your specific product and competitive landscape. Counsel can help map the optimal sequence based on your business model.

What This Means For You

Insurance is one of the harder industries for vibe coders to enter, but the rewards for those who navigate it successfully are substantial.

- If you're a founder considering insurance tech: Plan for 12 to 18 months to first revenue and accept the compliance overhead. Or pick an insurance-adjacent path with shorter timelines.

- If you're changing careers into insurance tech: The combination of technical skill and regulatory awareness is rare and valuable. Insurance tech roles pay well for hybrid skills.

- If you're a student: Read the basics of insurance regulation even if you do not work in insurance. The patterns generalize to other heavily-regulated industries.

Browse more regulated industry guides

Read more pulse articles