Vibe coding for fintech regulatory requirements in 2026 means navigating four common frameworks (PCI DSS, SOC 2, AML/KYC, money transmitter licensing) plus jurisdiction-specific rules, and understanding that regulators do not care whether your code was written by humans or AI as long as the resulting system meets the same standards. The shortcut for most early-stage fintechs is to build on a banking-as-a-service (BaaS) provider that handles licensing and most compliance, focus your engineering on the customer-facing experience, and only graduate to direct regulatory relationships when scale justifies the overhead. Done this way, fintech compliance becomes a 4 to 8 week setup rather than a 12-month project.

This piece walks through the four frameworks, the BaaS shortcut that most modern fintechs use, the engineering disciplines that satisfy regulators regardless of code authorship, and the four pitfalls that turn AI-built fintechs into regulatory case studies and how to avoid each one.

The frameworks described here cover US fintech specifically; international fintechs need similar work for their local regulators (FCA in the UK, BaFin in Germany, MAS in Singapore) but the principles are largely the same.

Why Regulators Do Not Care About AI Specifically

A common founder fear is that regulators will scrutinize AI-built fintech more harshly than human-built fintech. The 2026 reality is the opposite: regulators care about outcomes and processes, not authorship. A fintech app with proper audit trails, separation of duties, and risk controls passes review whether the code was written by Cursor, Copilot, or a human team. A fintech app missing those controls fails review regardless of authorship.

The reason this matters for vibe coders is that the compliance work is the same as it always was. AI did not invent new compliance requirements; it just changed who can build the underlying app fast enough to actually launch. The bottleneck for fintech in 2026 is still compliance, not engineering, which means the AI productivity gain compounds only when you also have the compliance work figured out.

A 2025 Treasury Prime survey of 300 fintech compliance officers found that none reported any specific concern about AI-generated code compared to human-generated code, as long as the surrounding controls (audit logs, testing, review processes) were in place. The compliance officers' top concerns were the same as a decade ago: AML/KYC effectiveness, transaction monitoring quality, and incident response readiness. AI is invisible to the regulator if the controls work.

The pattern to copy is the way fintechs handled the introduction of cloud computing. Regulators initially worried that cloud was inherently less secure than on-premises. Within a few years, the conversation shifted to "show us your cloud security controls" and the question of whether to use cloud became uninteresting. AI is on the same trajectory, faster.

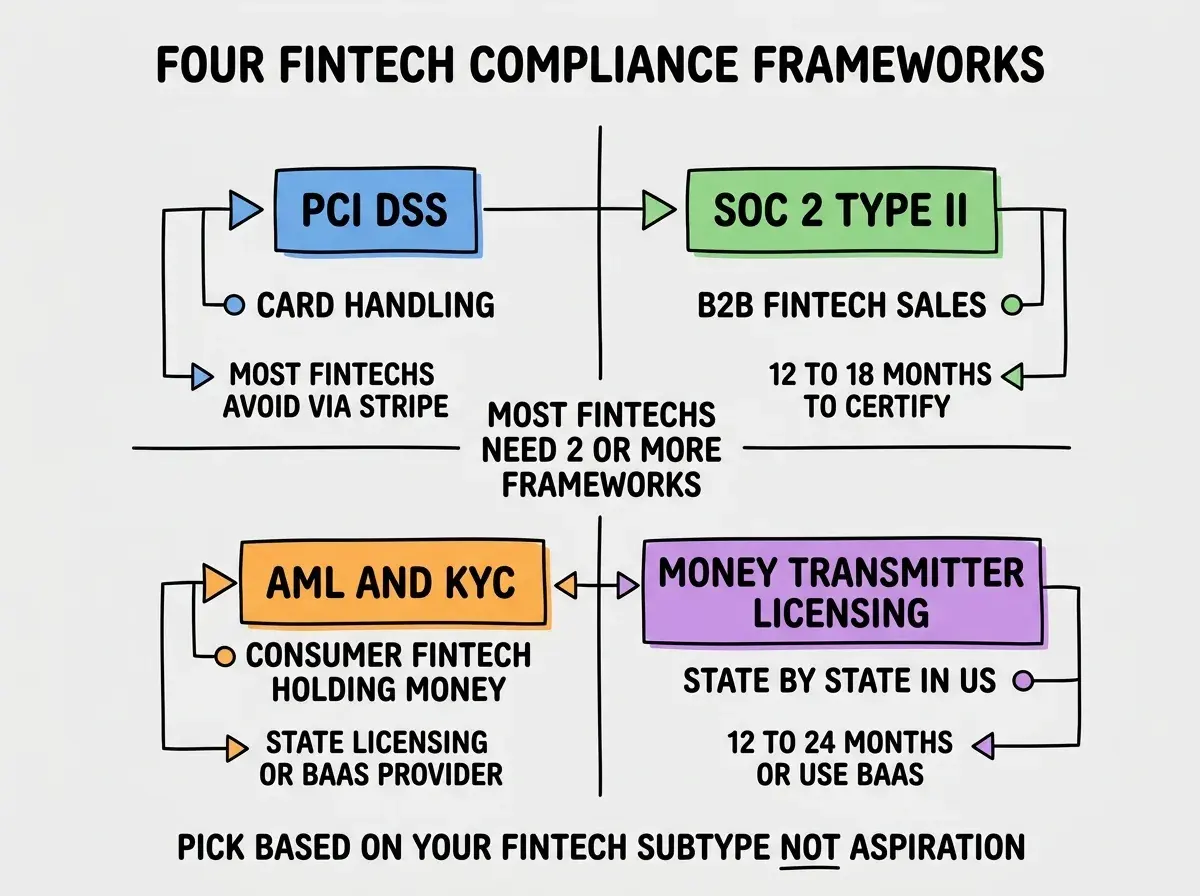

The Four Common Frameworks

Each framework applies to a specific subset of fintech work. Most fintechs need at least two of them.

PCI DSS. Required if you store, process, or transmit cardholder data. Most modern fintechs avoid PCI by using Stripe, Adyen, or similar processors that handle the cards directly. If you need to be in PCI scope, the work is substantial (3 to 6 months for SAQ-D level).

SOC 2 Type II. Table stakes for selling fintech to enterprise buyers. Plan for 12 to 18 months total: 6 months of building controls, 6 months of demonstrated operation, then the audit. Most B2B fintechs have this.

AML/KYC. Required for any fintech that holds customer money or facilitates transfers. Includes identity verification, transaction monitoring, suspicious activity reporting. Tools like Persona, Alloy, or Sardine handle most of the operational work.

Money transmitter licensing. Required state-by-state in the US for direct money handling. 12 to 24 months and $1M+ to acquire all 50 state licenses, or use a banking-as-a-service provider that has them.

The BaaS Shortcut Most Modern Fintechs Use

Banking-as-a-service providers (Lithic, Unit, Bond, Synctera, Treasury Prime, others) handle the heaviest compliance lifting in exchange for a percentage of revenue or per-transaction fees. The trade-off is real and worth understanding.

What BaaS providers handle. Money transmitter licensing, banking partner relationships, AML/KYC operations, transaction monitoring, OFAC screening, regulatory reporting. Essentially the entire regulatory back end.

Browse more analysis on regulated industries

Browse pulse articlesWhat you still own. The customer-facing app, your privacy policy, fraud detection at the application layer, customer support, and any value-add services beyond core banking. This is plenty of work but it is engineering work you can do.

The cost trade-off. BaaS typically takes 0.5 to 2 percent of revenue or interchange. For early-stage fintechs this is dramatically cheaper than building the regulatory back end yourself. For mature fintechs at scale, the math may flip toward direct relationships, but the transition is years away for almost everyone.

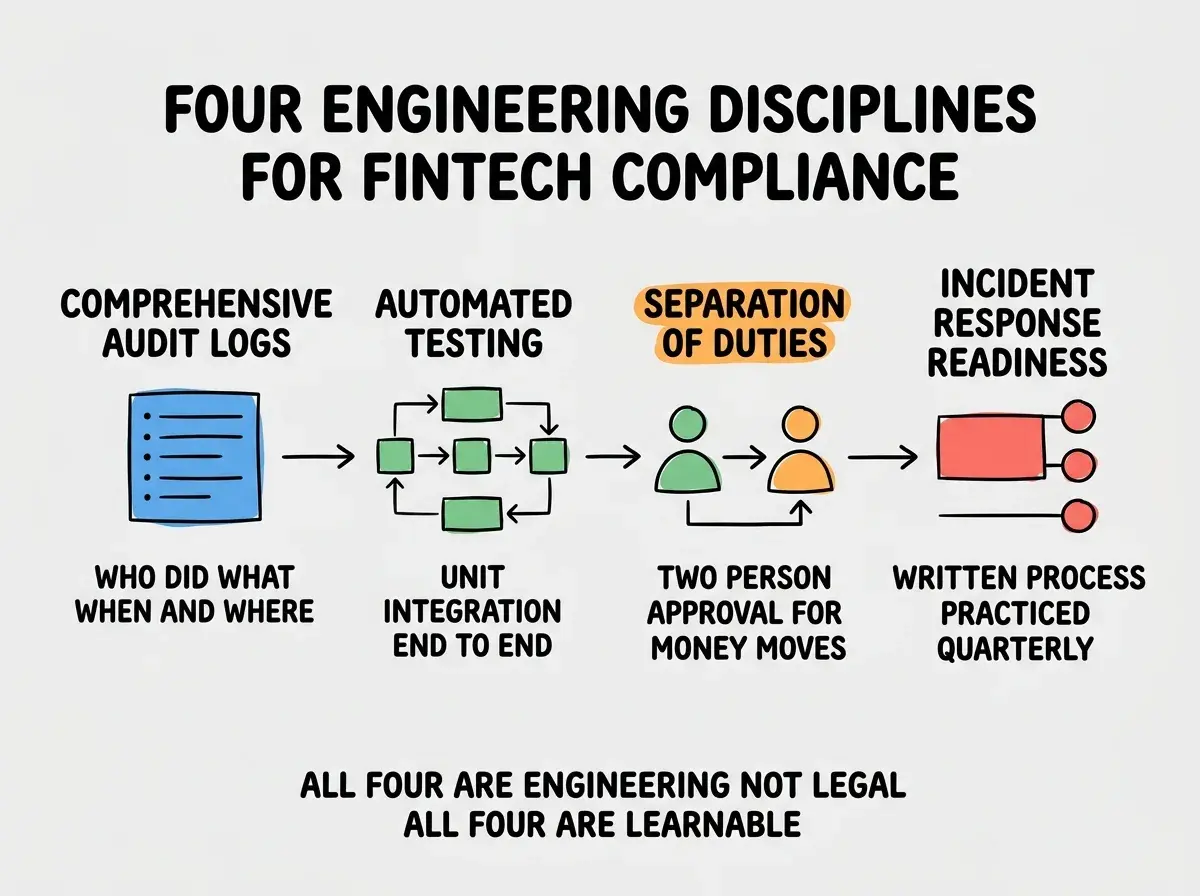

The Engineering Disciplines That Satisfy Regulators

Regardless of BaaS or direct relationships, four engineering disciplines satisfy regulators consistently in fintech.

Discipline 1, comprehensive audit logs. Every action that affects money or customer data is logged with full context. This is the single most-asked-about control in fintech audits.

Discipline 2, automated testing. Unit, integration, and end-to-end tests covering the critical money-moving paths. Manual testing alone is insufficient for fintech.

Discipline 3, separation of duties. Two-person approval for any transaction above a threshold. Code-level enforcement that the same user cannot both initiate and approve.

Discipline 4, incident response readiness. Written incident response plan, practiced quarterly via tabletop exercises. Regulators want to see that you would handle a real incident competently, not just that you have a document on the shelf that nobody has read since it was written.

The most expensive fintech compliance mistake is treating it as a one-time gate before launch. Compliance is an ongoing program: every new feature requires updated risk assessment, every quarter requires reviews, every annual cycle requires SOC 2 re-audits. Building the compliance discipline into the product development cycle from day one is much cheaper than trying to bolt it on after each major release. The teams that get this right ship faster than the teams that treat compliance as periodic overhead.

The other mistake is assuming BaaS providers will protect you from your own mistakes. They handle the regulatory back end but they do not handle bugs in your app, fraud at your customer interface, or poor customer support. The compliance partnership is real but it is not a free pass.

A useful diagnostic during the BaaS evaluation is to ask each potential provider for a list of specific compliance items they own versus items you own. The good providers have this written down clearly. The weak providers wave their hands. Picking a provider with a clear ownership boundary saves you from discovering during an audit that something you assumed was covered actually was not.

What This Means For You

Fintech compliance with AI-built code is no different from fintech compliance with human-built code. The frameworks, the controls, and the processes are the same; AI just makes the underlying engineering faster.

- If you're a founder: Use a BaaS provider for v1 unless you have specific reasons to handle licensing directly. The speed-to-market gain is enormous and the cost is reasonable for early stages.

- If you're changing careers: Fintech compliance engineering is a defensible specialization with strong demand and high pay. The barrier to entry is real but learnable.

- If you're a student: Study one fintech compliance framework deeply (SOC 2 transfers most broadly). The patterns apply to many other regulated industries.

Browse more analysis on regulated industries

Browse pulse articles