If your vibe-coded app takes payments, PCI compliance for your web app is not optional. With 92% of builders using AI tools daily, the good news is that modern payment providers handle most of the hard parts. But 45% of AI-generated code contains security vulnerabilities, and payment flows are where those flaws cost real money.

What PCI DSS Actually Means in Plain English

PCI DSS stands for Payment Card Industry Data Security Standard. It is a set of rules created by Visa, Mastercard, American Express, Discover, and JCB to protect cardholder data. If your application accepts, processes, stores, or transmits credit card information, PCI DSS applies to you.

The standard has 12 core requirements covering everything from network security to access control to regular testing. Reading the full specification feels like reading a legal contract written by security engineers. It is not designed for indie hackers shipping their first SaaS.

Here is what it boils down to. You must protect cardholder data wherever it exists in your system. You must restrict who and what can access that data. You must regularly test that your protections work. And you must document all of it.

The consequences of non-compliance are real. Fines range from $5,000 to $100,000 per month. Your payment processor can terminate your account. If a breach occurs, you are liable for the cost of every compromised card, averaging $150 per record.

PCI compliance is not a certification you apply for. It is a set of requirements you must continuously meet. The simplest path for vibe-coded apps is to never let card data touch your servers at all. Use Stripe Checkout, Lemon Squeezy, or a similar hosted payment form, and your compliance scope shrinks dramatically.

Why Stripe and Lemon Squeezy Handle Most of the Hard Parts

The single most important concept in PCI compliance for web apps is tokenization. When you use Stripe Checkout, Stripe Elements, or Lemon Squeezy's hosted payment overlay, the credit card number never touches your server. The user enters card details into a form hosted entirely by the payment provider, running in a separate iframe or domain. Your server only ever receives a token, a random string that represents the payment method.

This is not a technicality. It fundamentally changes your compliance requirements.

Stripe is a PCI Level 1 Service Provider, the highest certification level. They handle all the encryption, storage, and transmission of actual card numbers. When you use their hosted payment solutions, they take on the liability for cardholder data protection. Your application never sees a real credit card number, which means most of the 12 PCI requirements simply do not apply to you. Lemon Squeezy works the same way with their checkout overlay.

This is why every experienced developer will tell you the same thing. Do not build your own payment form. Use the hosted solution from your payment provider. It is faster to implement, more secure, and dramatically reduces your compliance burden.

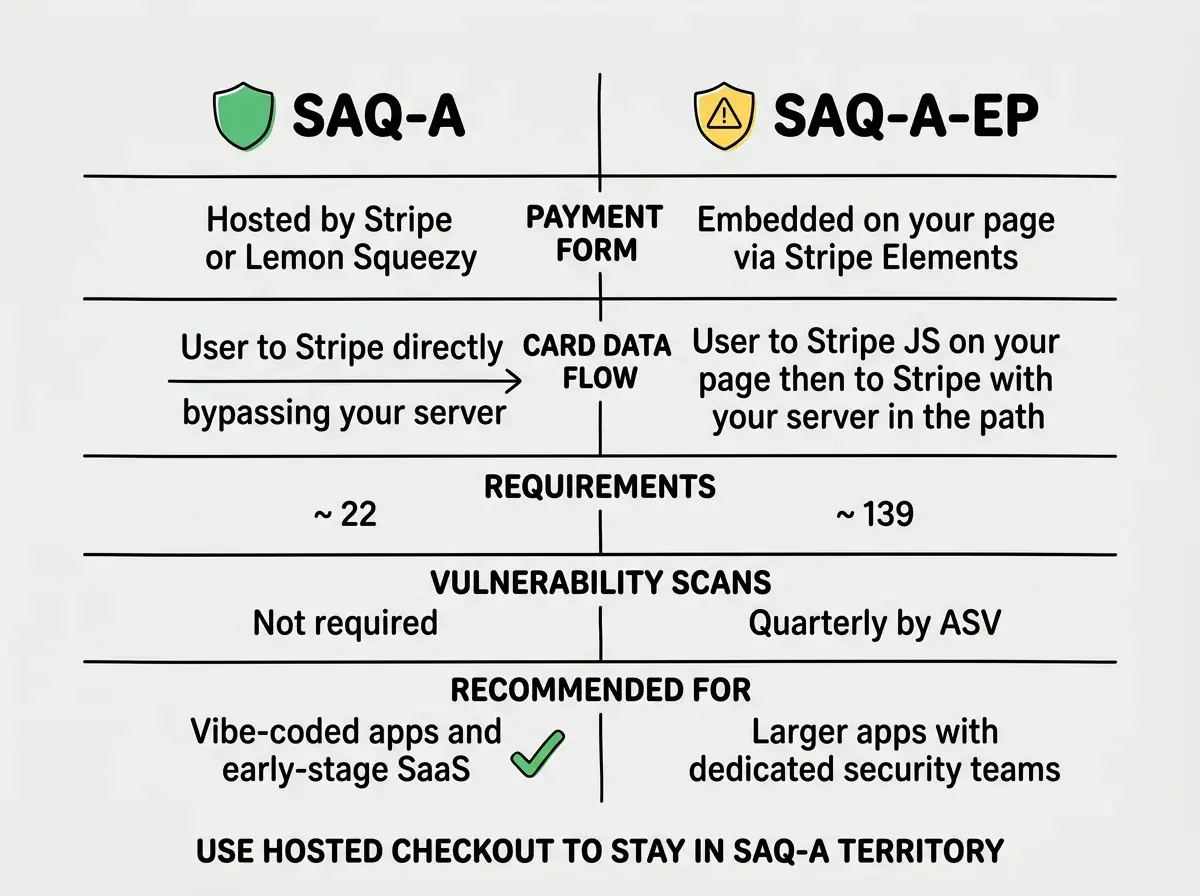

SAQ-A vs SAQ-A-EP and Why It Matters

PCI compliance is verified through Self-Assessment Questionnaires (SAQs). Which questionnaire applies to you depends on how your application handles payment data.

SAQ-A is the simplest. It applies when your application fully outsources all payment processing to a PCI-compliant third party. If you use Stripe Checkout (the redirect or hosted payment page) and card data never touches your servers, you qualify for SAQ-A. It has about 22 requirements. Most of them are administrative, like confirming that you use HTTPS and that you have a security policy.

SAQ-A-EP is more involved. It applies when your application hosts the payment page but uses JavaScript from the payment provider (like Stripe Elements embedded in your own page) to collect card data. Even though card numbers go directly to Stripe via their JavaScript library, your server serves the page containing the payment form. A compromised server could inject malicious JavaScript to intercept card data. SAQ-A-EP has about 139 requirements and includes vulnerability scanning.

The practical difference is significant. SAQ-A means a short annual form. SAQ-A-EP means quarterly vulnerability scans by an Approved Scanning Vendor, formal penetration testing, and documented security policies. For vibe-coded apps, use Stripe Checkout (redirect mode) or Lemon Squeezy's hosted overlay to stay in SAQ-A territory.

What Is Still Your Responsibility

Even with Stripe handling all card processing, several PCI requirements still apply to your application.

HTTPS everywhere. Your entire application must be served over HTTPS, not just payment pages. Every major hosting provider (Vercel, Cloudflare, Netlify) provides free SSL certificates. If any page on your domain loads over HTTP, you fail this requirement.

No card numbers in logs, databases, or error messages. AI-generated code frequently logs entire request bodies for debugging purposes. If a user somehow submits card data to your server, and your application logs the request body, you just stored cardholder data in your log files. Search your codebase for any logging that captures raw request data.

Access control. Limit who can access your payment provider's dashboard, API keys, and webhook secrets. Enable two-factor authentication on your Stripe or Lemon Squeezy account. Do not share API keys in Slack, email, or Git repositories.

Webhook verification. When Stripe sends a webhook to your server confirming a payment, you must verify that it actually came from Stripe by checking the cryptographic signature in the webhook headers. Without verification, an attacker can send fake payment confirmations and get access to paid features without paying.

Payment Security Mistakes AI Tools Make

AI coding tools are particularly bad at payment integrations because payment security requires context beyond "make it work." Here are the patterns I see repeatedly.

Storing card data directly. I have seen AI tools generate forms that collect card numbers in regular input fields and submit them to the application's own backend. The AI solves the stated problem (collect payment information) without understanding that you should never do this. If you see <input name="cardNumber"> submitting to your own API route, stop immediately and replace the flow with Stripe Checkout.

Skipping webhook signature verification. AI tools consistently generate webhook handlers that parse the request body and process it without verifying the stripe-signature header. Anyone can POST a fake event to your webhook endpoint and trigger whatever logic follows a successful payment. Every Stripe SDK provides a constructEvent method that verifies the signature. Use it. Always.

Hardcoding API keys. AI tools drop Stripe secret keys directly into source code instead of reading them from environment variables. If that code gets committed to a Git repository, your Stripe keys are compromised. An attacker with your secret key can issue refunds, create charges, and access all your customer data.

The most dangerous AI payment pattern is building a custom checkout form that collects card data on your server. It technically works, it processes payments successfully, and it puts you in scope for the full PCI DSS assessment (300+ requirements). Always use Stripe Checkout, Stripe Elements, or a hosted payment overlay. Never let card numbers touch your server.

Missing error handling on payment failures. AI-generated payment code handles the happy path (payment succeeds) and ignores every failure mode. Failed charges, expired cards, 3D Secure challenges, and network timeouts all need explicit handling. When these fail silently, users get charged without receiving access, or get access without being charged.

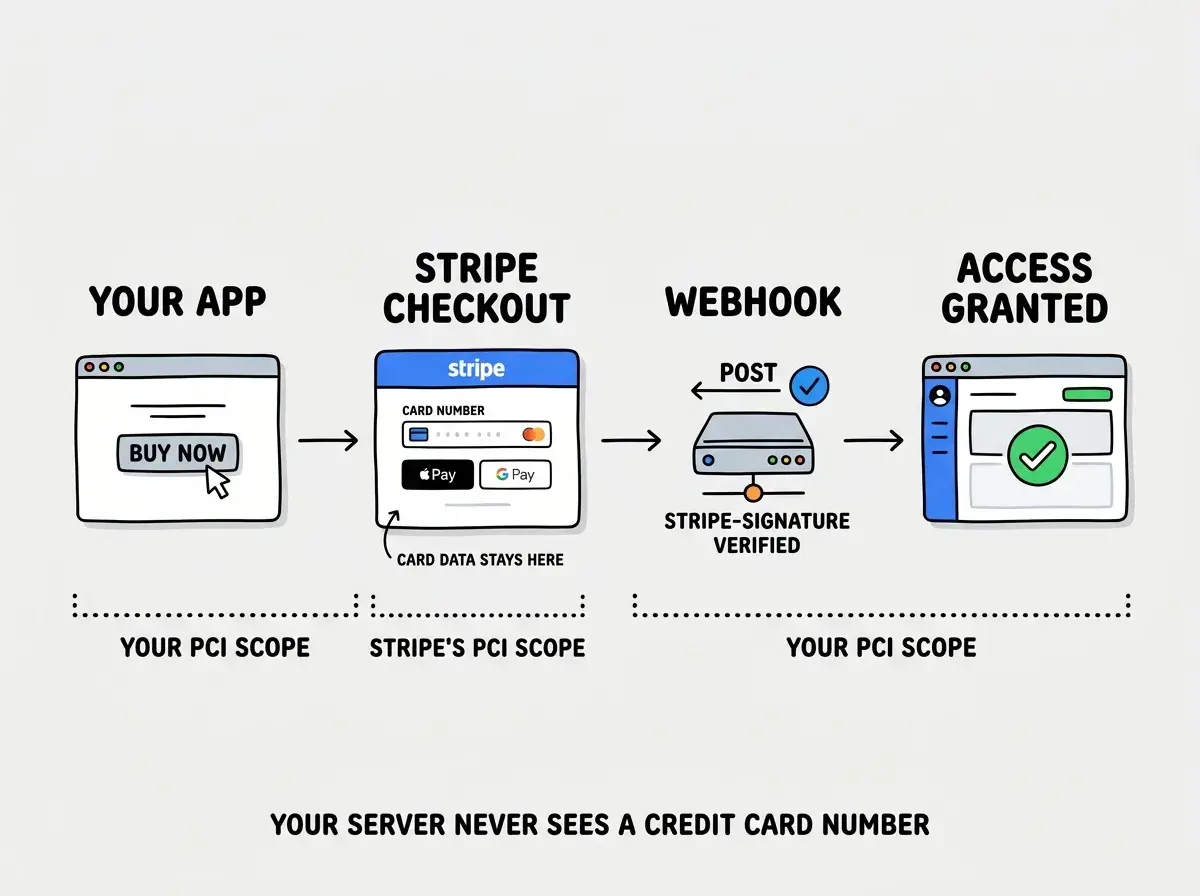

Stripe Checkout Is the Safest Path

For vibe-coded applications, Stripe Checkout in redirect mode is the optimal choice. Here is why.

You create a Checkout Session on your server with the price and success/cancel URLs. Stripe redirects the user to a Stripe-hosted payment page. After payment, Stripe redirects back to your success URL. A webhook confirms the payment on your server. At no point does your server handle card data.

This gives you SAQ-A compliance, built-in 3D Secure authentication, Apple Pay and Google Pay support, and fraud detection through Stripe Radar. All without writing payment form code. The user briefly leaves your site, but Stripe's hosted checkout conversion rates are actually higher than most custom forms.

Get the complete guide to shipping secure, production-ready applications with AI tools.

Read the shipping guideThe Compliance Checklist for Vibe-Coded Payment Apps

Before you ship any application that accepts payments, run through this list.

- All payment data collection happens on a Stripe or Lemon Squeezy hosted form, never on your own server

- Your entire application is served over HTTPS with a valid SSL certificate

- Webhook endpoints verify the cryptographic signature before processing any event

- Stripe secret keys and webhook signing secrets are stored in environment variables, never in source code

- Your application logs do not capture raw request bodies that could contain card data

- Your Stripe dashboard has two-factor authentication enabled

- Failed payment scenarios are handled explicitly with appropriate user feedback

- Your Git history does not contain any payment API keys (run

gitleaksortrufflehogto verify)

If you can check every box, you are meeting the core PCI DSS requirements for a SAQ-A merchant. No security consultant needed. No penetration test required. Use hosted checkout, verify your webhooks, and keep your keys out of your code.

45% of AI-generated code has security flaws. Find yours before your users do.

Get the security checklistWhat This Means For You

PCI compliance sounds intimidating, but for vibe-coded apps it reduces to one core principle. Never let credit card data touch your server. Use Stripe Checkout or Lemon Squeezy's hosted payment flow, verify your webhooks, serve everything over HTTPS, and keep your API keys in environment variables. That covers the vast majority of what PCI DSS requires for your compliance level. The payment providers spent years and millions of dollars building secure payment infrastructure so you do not have to. Use what they built. Ship your product. Focus on what differentiates your business, not on reinventing payment security.