To build a fintech dashboard with compliance in mind in 2026, you need to know which of the four common frameworks apply to your product (PCI DSS, SOC 2, ISO 27001, AML/KYC), implement audit trails for every money-affecting action, design clear separation between read-only and money-moving permissions, and accept that the compliance work is roughly 30 to 40 percent of the total build time. The dashboard UI itself is a normal data visualization app that AI tools handle well; the compliance posture is what makes the difference between a product that ships and one that stalls in vendor security reviews.

This piece walks through which frameworks apply to which fintech subtypes, the audit trail architecture that holds up under review, the permission model that prevents costly mistakes, and the four pitfalls that delay most fintech launches by months and that are entirely preventable.

Why Fintech Compliance Is Different From Other Verticals

Fintech compliance is uniquely demanding because money is fungible and irreversible. A healthcare data leak is bad; a fintech bug that moves money to the wrong account is worse, because the money may not come back. The compliance frameworks have evolved to require multiple safeguards (audit trails, approval workflows, transaction reconciliation) that you do not need for non-financial apps.

The other difference is that fintech customers (banks, payment processors, large enterprises) require extensive vendor security reviews before they will integrate with you. Without SOC 2 Type II in hand, you cannot sell to most enterprise fintech buyers. The compliance work is not just regulatory; it is part of the go-to-market motion.

A 2025 Lithic survey of 200 fintech startups found that 67 percent of pre-revenue startups underestimated their compliance work by at least 50 percent, and the median fintech took 4 to 8 weeks longer to reach launch than they planned because of compliance reviews. Companies that planned for compliance from the start launched on schedule; companies that treated it as a "we will handle that later" item consistently slipped. Compliance is not optional in fintech; it is a planning input.

The pattern to copy is the way commercial airlines handle pre-flight safety. Every flight, regardless of how routine, follows the same checklist before takeoff. The captain does not skip checks because they have done this route 1,000 times. Fintech compliance is the same; every change to the system goes through the same review process because the cost of failure is high enough to justify the overhead.

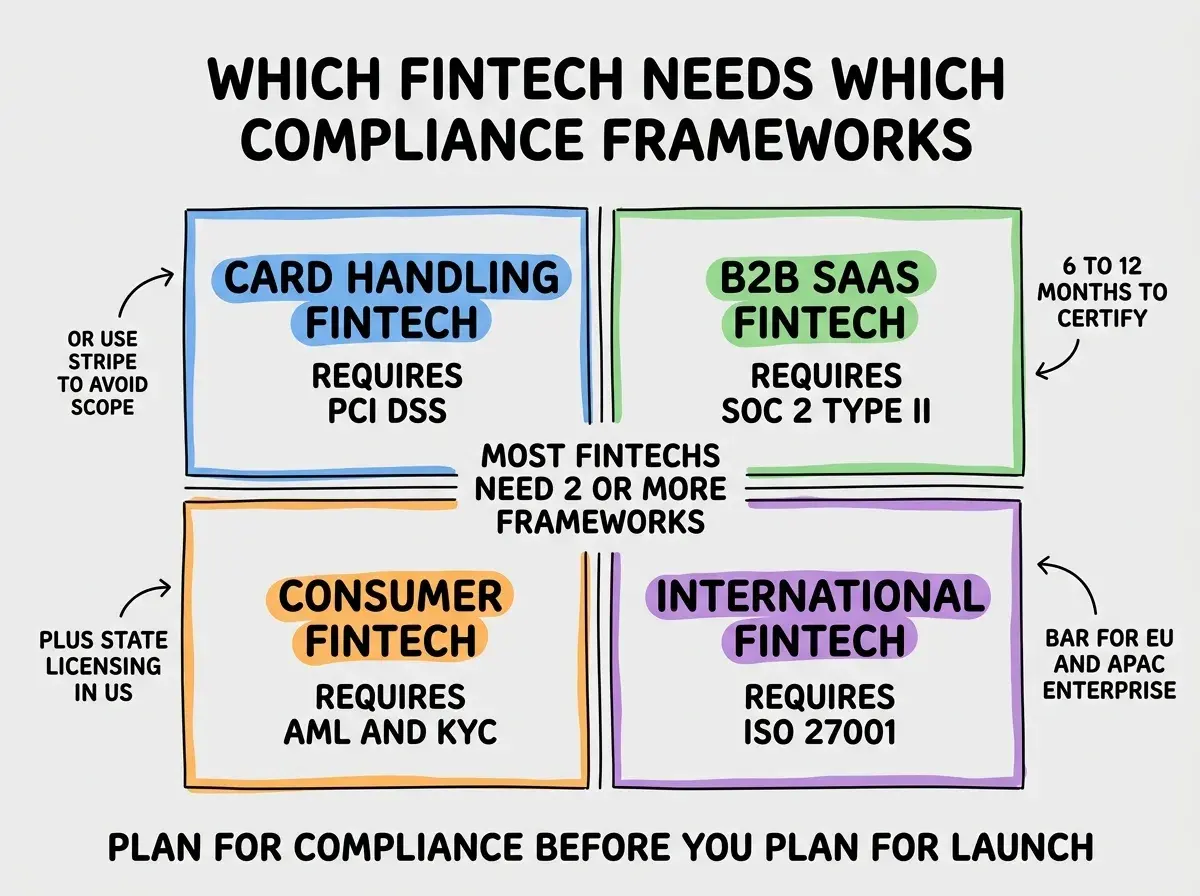

Which Frameworks Apply to Which Fintech Subtypes

The four common frameworks are PCI DSS (handling card data), SOC 2 (general security and availability), ISO 27001 (international information security), and AML/KYC (anti-money laundering / know your customer). Different fintech subtypes require different combinations.

Card-handling fintech. PCI DSS is required if you store, process, or transmit cardholder data. Most modern fintechs avoid PCI by using Stripe, Adyen, or similar to handle the cards directly, which scopes you out of PCI.

B2B SaaS fintech. SOC 2 Type II is the table stakes for selling to enterprise buyers. Plan for 6 to 12 months from start to certification, with a pre-audit period of 6 months minimum.

Consumer fintech. AML/KYC is required for any product that holds customer money or facilitates transfers. Plus state-level money transmitter licensing in the US (or use a banking-as-a-service provider that has the licenses).

International fintech. ISO 27001 is the bar for selling into EU and APAC enterprise markets. Often paired with SOC 2 since they overlap substantially.

The Audit Trail Architecture

Audit trails are non-negotiable in fintech and the design choice has consequences for years. Three patterns work well in 2026.

Append-only event log. Every money-affecting action (transfer initiated, transaction approved, balance updated) writes an immutable event to a log. Reads of the current state derive from the event log via projection. This is the cleanest pattern and what most modern fintechs adopt.

Browse more domain-specific build guides

Read more build articlesDatabase with explicit audit table. Simpler alternative if event sourcing is overkill. A separate audit_log table records every money-affecting database write, with timestamp, user, action, before/after values, and approval chain.

Third-party audit logging service. Datadog, Splunk, or a dedicated service like Cribl handles the audit log infrastructure. Useful for teams that want to outsource the compliance posture but are comfortable with the cost.

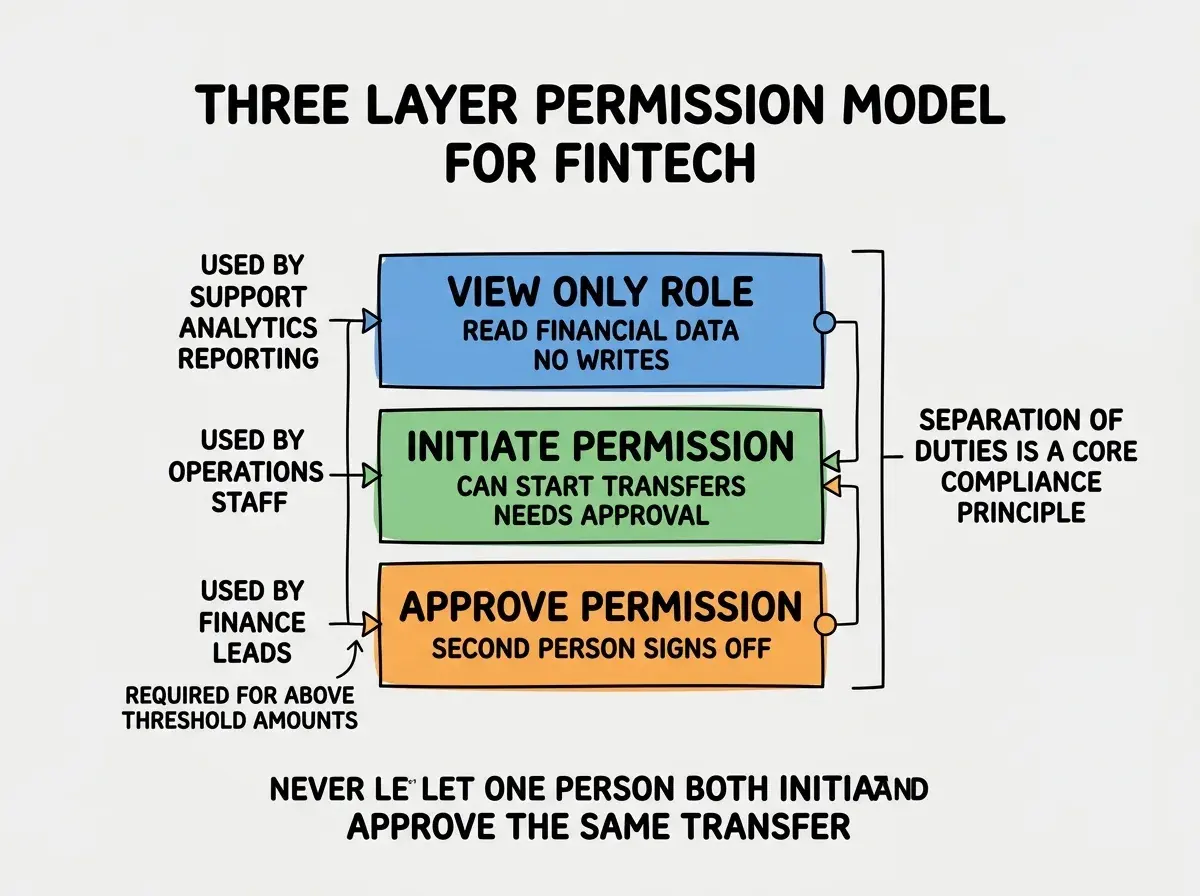

The Permission Model That Prevents Disasters

Fintech permission models are stricter than typical SaaS. Three layers prevent most costly mistakes.

View-only role. Most users only need to view financial data, not move money. Support staff, analytics, executives reading reports. This role has no money-moving capabilities at all.

Initiate permission. Staff who can start transfers or transactions but cannot approve them alone. Operations team, finance team. Their actions go into a queue requiring approval.

Approve permission. Senior staff who approve transfers initiated by others. Required for any transaction above a defined threshold (e.g., $10,000). Requires a different person than the initiator.

The most damaging fintech mistake is allowing one person to both initiate and approve the same transaction. This violates the separation of duties principle, fails most compliance audits, and creates the opening for both fraud and honest mistakes. Implement two-person approval for any money-moving action above a threshold from day one. The friction is small for legitimate operations and the protection from disasters is substantial. Many fintech failures (insider fraud, mistaken transfers) trace back to this single gap.

The other mistake is over-relying on the application layer for compliance. Application code can have bugs; database constraints and infrastructure controls are harder to bypass. Implement permission checks both in the app code and as database row-level security or stored procedure constraints. The redundancy catches issues that single-layer checks miss.

A useful exercise during architecture is to map every money-affecting action against the four compliance frameworks and note which controls each action requires. Most fintechs find that 80 percent of actions need only basic audit logs while 20 percent need full approval workflows. This mapping becomes the compliance test plan and prevents the situation where a new feature ships without the right controls because nobody remembered to check.

A second small habit is to keep a fintech compliance diary where you log every regulatory question that came up during a product decision and how you resolved it. After a year, the diary becomes a training resource for new engineers and a reference for SOC 2 auditors. Most teams underestimate how much institutional knowledge accumulates around compliance decisions, and writing it down protects against losing it when the original decision-maker leaves.

What This Means For You

Fintech compliance is real work, but it is also the moat that protects fintech businesses from casual entrants. Building it in from day one is dramatically cheaper than retrofitting and is itself a competitive advantage.

- If you're a founder: Plan for compliance as a 30 to 40 percent share of your build budget and timeline. The cost is real and predictable; surprise is expensive.

- If you're changing careers: Fintech compliance expertise is one of the best-paid specializations in tech. The barrier to entry is high but the demand is steady.

- If you're a student: Study one compliance framework deeply (SOC 2 is most transferable). The principles apply to every regulated vertical you might work in.

Browse more domain-specific build guides

Read more build articles